As President-elect Donald Trump prepares to reenter the White House, his campaign promise to reshape or dismantle the Affordable Care Act (ACA) is back in the spotlight.

For a man who has branded the ACA as a government overreach, the irony is thick: the very states that propelled him to victory and have the highest ACA enrollment rates are poised to bear the brunt of any cuts or policy rollbacks.

Promises of “Reform” and a Familiar Target

Trump and his Republican allies have long criticized the ACA, branding it as a bloated and ineffective program. During his first term, the administration eliminated the individual mandate’s tax penalty, a cornerstone of the ACA.

Now, with control of both the House and Senate, Republicans are once again poised to take a scalpel or a sledgehammer to the health care law.

House Speaker Mike Johnson has called for “massive reform,” while others have hinted at more subtle ways to undermine the ACA. But whether through sweeping legislation, executive orders, or sheer neglect, the implications are clear: millions of Americans could lose their health insurance, and the uninsured rate, which hit record lows under the ACA, could spike dramatically.

The States Most at Risk: Trump Country

Here’s the kicker: the ACA has become a lifeline for millions of residents in red states.

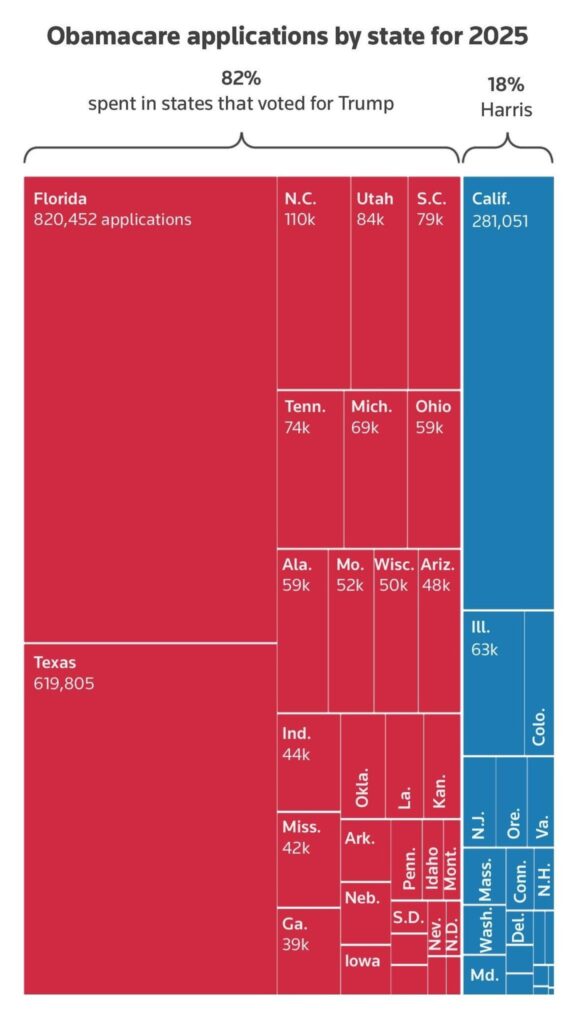

According to Reuters, 82% of ACA applications for 2025 are from states that voted for Trump in the 2024 election. These include Florida, Texas, and North Carolina, which lead the nation in ACA enrollments. Yet these states also stand to lose the most if federal subsidies and protections are rolled back.

Consider this: the subsidies that have helped make ACA plans affordable for middle-class families are set to expire in 2025. Without congressional action, premiums could double or even triple, pricing many out of coverage entirely.

The Congressional Budget Office (CBO) estimates that nearly 4 million people could lose their insurance by 2026.

“Repeal with a Different Name”

The GOP’s approach to dismantling the ACA ranges from outright repeal to death by a thousand cuts. As Cynthia Cox of the Kaiser Family Foundation (KFF) put it, these plans amount to “repeal with a different name.”

Proposals include:

- Changing Medicaid Funding: By reducing federal contributions for Medicaid expansion, states could face funding shortfalls, leading to stricter eligibility requirements. This would disproportionately affect low-income adults without children, a significant portion of Medicaid recipients in red states.

- Subsidy Changes: Republicans have floated the idea of allowing ACA subsidies to be used for plans that don’t comply with ACA standards. While these plans might be cheaper, they often offer minimal coverage, leaving older and sicker individuals to shoulder higher premiums.

- Inaction: Letting enhanced subsidies expire would effectively dismantle much of the ACA’s progress without passing a single bill. Premiums would soar, and millions could lose coverage.

A Familiar Playbook: Executive Orders and Waivers

If Congress hesitates, Trump has another tool in his arsenal: executive action.

During his first term, Trump’s Department of Health and Human Services (HHS) encouraged states to apply for waivers to restructure Medicaid. These waivers allowed states to impose work requirements and cap federal funding policies that often resulted in reduced coverage.

“Trump will do whatever he thinks he can get away with,” said Chris Edelson, an assistant professor of government at American University.

“If he wants to do something, he’ll just do it.”

This time, Trump could also use executive orders to expand short-term health plans, often derided as “junk insurance” because they lack ACA-mandated protections, such as coverage for preexisting conditions.

During the Biden administration, these plans were curtailed. A Trump White House would likely reverse those restrictions, prioritizing market freedom over comprehensive coverage.

Collateral Damage: Preventive Care and Beyond

One of the ACA’s most popular provisions requires insurers to cover preventive services, such as cancer screenings and vaccinations, at no cost to patients. But this mandate is already under legal threat.

If the Trump administration withdraws its defense of the law, it could pave the way for broader challenges, potentially leaving millions without access to affordable preventive care.

Dylan Reed, a small-business owner from Colorado, is among those worried. Reed relies on his ACA plan to manage multiple chronic conditions, including scleroderma and ADHD. “It’s definitely a terrifying thought,” he said.

“I would probably survive. I would just be in a lot of pain.”

Budget Cuts: Musk, Ramaswamy, and the Irony of “Trump Country”

The broader budgetary context adds another layer of irony.

As Reuters reported, Trump has enlisted Elon Musk and Vivek Ramaswamy to identify cuts to federal programs. Among the targets?

Medicaid, SNAP benefits, and even veterans’ programs initiatives that disproportionately benefit residents of red states.

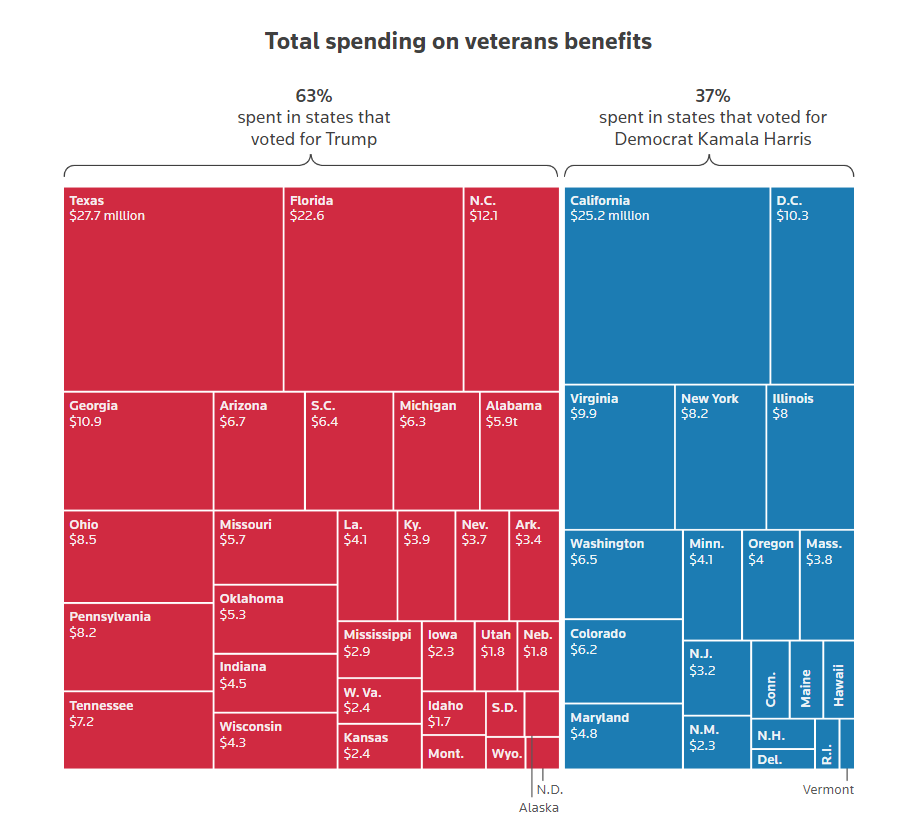

Graphics from Reuters highlight the stark divide: 63% of federal spending on veterans’ benefits goes to states that voted for Trump in 2024.

Yet these same programs could see reductions under his administration. Similarly, cuts to Medicaid and SNAP would hit hardest in states like Louisiana, where poverty rates are high and government aid plays a crucial role.

Political Realities and Public Backlash

Despite the rhetoric, dismantling the ACA won’t be easy. Republicans learned this lesson the hard way in 2017, when their repeal efforts failed amid public outcry and defections within their own ranks.

Polls consistently show that key ACA provisions, such as protections for preexisting conditions, remain overwhelmingly popular.

“The ACA will survive, but only a bare-bones version,” said Lawrence Gostin, director of the O’Neill Institute for National and Global Health Law at Georgetown University.

But the potential backlash doesn’t seem to faze Trump’s team. “If Republicans control the House, the Senate, and the presidency, then we might see a repeat of 2017,” Cox warned.